Lease a Car: Quick Tips

- Considering your annual mileage is a crucial step when leasing a car.

- Negotiate when leasing to reduce the capital cost and money factor, which will lower your monthly payment.

- Get familiar with leasing jargon because some terms aren’t used in traditional auto financing.

- Establish and stay within a budget. Remember that you are responsible for maintenance and insurance expenses for a leased car.

At first blush, car leasing seems like a grand idea. After all, you can get more car for the same monthly financing payment. But a lower payment is only one part of the decision.

Many shoppers lease because they like driving a new vehicle every two or three years, staying under warranty, or simplifying business-use deductions. Automakers may also offer lease incentives that are not available on purchases. And when the lease ends, you can usually return the vehicle without selling it or negotiating a trade-in.

This guide explains how leasing works, what you can negotiate, how leasing compares with buying, and what to know before signing.

- What Is Car Leasing?

- What to Know Before Leasing

- Negotiating Lease Costs

- Leased Car Maintenance

- Insuring a Leased Car

- Terminating a Lease Early

- How Does Credit Affect Car Leasing?

- Car Leasing vs. Buying

- Differences Between Leasing and Buying

- Types of Leases

- How Long Is a Car Lease?

- Leasing Terminology to Know

- How to Lease a Car

- Bottom Line on Car Leasing

What Is Car Leasing?

Car leasing is like renting a vehicle for a contracted period, usually 24 to 36 months. Unlike financing a purchase, where payments help you eventually own the car, leasing means you pay for the vehicle’s estimated depreciation during the lease term, plus financing charges.

Most consumer leases are closed-end leases. That means the lease sets the mileage limit, monthly payment, term, and purchase option upfront.

What Do You Need to Know Before Leasing?

The most important question is: How many miles do you drive each year?

Leasing Mileage Cap

Signing a lease means agreeing to a mileage cap, usually 10,000 to 15,000 miles per year. Exceed it, and the leasing company charges a per-mile penalty.

Penalties often range from 12 cents to 30 cents per excess mile. At 30 cents per mile, every additional 1,000 miles would cost you $300. Before signing, estimate your annual driving and confirm the mileage charge.

What Is the Money Factor in Leasing?

When you finance a car, the cost of borrowing is shown as an interest rate. In a lease, that cost is called the money factor.

Money factors are shown as decimals, such as 0.0010 or 0.0023. To estimate the equivalent interest rate, multiply the money factor by 2,400. For example, 0.0023 x 2,400 = 5.5%.

Can I Negotiate the Price of a Leased Car?

Yes. You can negotiate the vehicle’s capitalized cost, which is the lease version of the purchase price. Manufacturer incentives or advertised lease deals may limit flexibility, but it is still worth asking.

TIP: Dealers may be more willing to negotiate before a new model arrives or near the end of the model year.

How Can I Reduce a Monthly Lease Payment?

- Reduce the capitalized cost by negotiating a lower vehicle price.

- Ask for a lower money factor, especially with strong credit.

- Put more money down or negotiate a higher trade-in value.

- Compare offers from multiple dealers.

What Can You Negotiate in a Lease?

- Capitalized cost

- Down payment

- Trade-in value

- Money factor

- Disposition fee

What Usually Cannot Be Negotiated?

- Residual value, which the leasing company generally sets

- Acquisition fee, which lessors rarely waive

Who Maintains a Leased Car?

You are responsible for maintaining the vehicle according to the owner’s manual. Some new vehicles include complimentary maintenance, which can reduce lease-term costs.

At the end of the lease, the leasing company inspects the vehicle for damage beyond normal wear and tear. If the inspector finds excess wear, you will be charged.

Who Insures a Leased Car?

You are responsible for the insurance coverage for the leased vehicle. The leasing company sets minimum coverage requirements, so confirm those amounts and get an insurance quote before signing.

What If I Want Out of My Lease Early?

A car lease is a binding contract. If you end it early, expect a penalty. In some cases, you may owe a large portion of the remaining payments. You cannot simply sell the car because you do not own it.

Market conditions may give you options. A dealership might help you exit a lease early if it wants your vehicle. Lease-transfer services may also connect you with someone willing to assume the lease, though fees may apply.

Compare all costs before choosing an early-exit option.

How Does Credit Affect Car Leasing?

As with financing, leasing companies review your credit score and history. Leasing generally requires stronger credit than financing because the lessee builds no equity in the vehicle.

If your credit score is low, you may still qualify, but expect a larger down payment and a higher money factor.

RELATED: Can I Buy a Car with Poor Credit History?

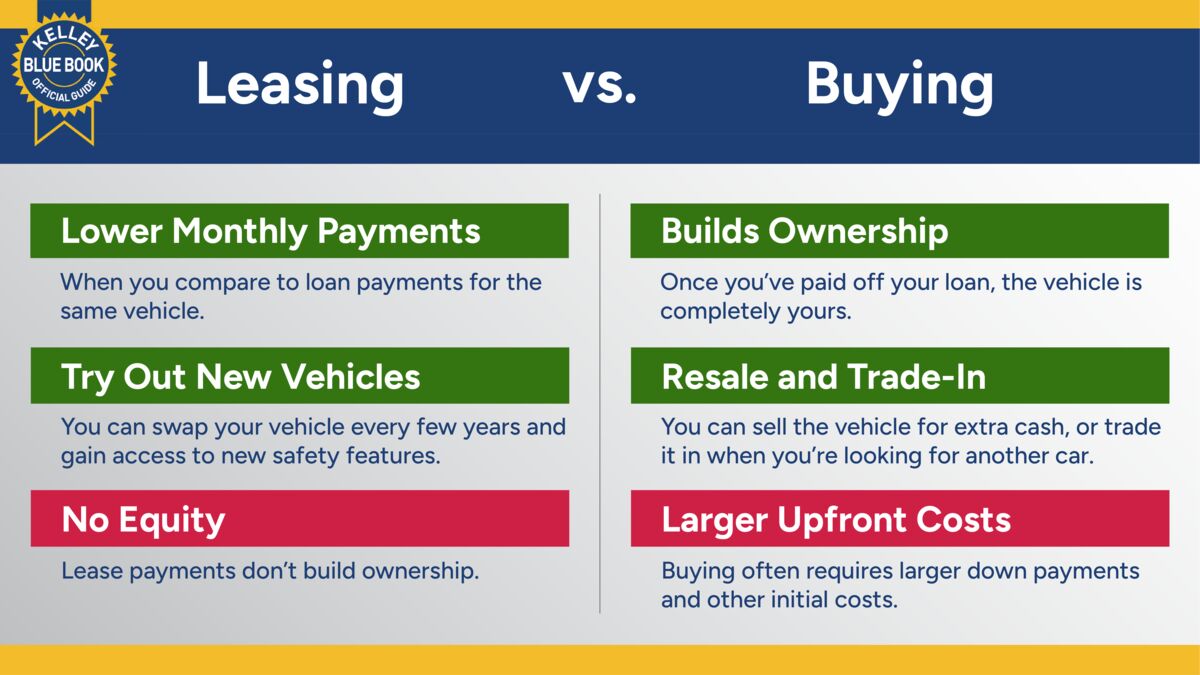

Car Leasing vs. Buying

Whether you lease or finance, you will likely make monthly payments and pay upfront fees. With financing, the upfront cost is usually a down payment. With leasing, you may pay a security deposit, first month’s payment, acquisition fee, down payment, taxes, registration, or some combination.

Pros of Leasing

- Lower monthly payment. Because you pay for estimated depreciation rather than the full purchase price, lease payments are usually lower than loan payments for the same vehicle.

- New vehicle every few years. Leasing lets you drive a newer vehicle more often, usually while it is still under the factory warranty. You may also benefit from newer safety and technology features.

- Easier end-of-term process. At lease end, you can usually return the car without selling it or negotiating a trade-in.

- Possible purchase opportunity. If the car is worth more than its residual value, buying it at lease end may be a good deal.

- Used-car leasing may be available. Some dealers lease certified pre-owned vehicles, usually newer models with warranty coverage.

RELATED: Returning a Lease Car: What To Expect

Cons of Leasing

- No equity. Lease payments do not build ownership value. At the end, you return the vehicle unless you buy it.

- Mileage limits. Every lease includes a mileage cap. Exceed it, and you pay a penalty. High-mileage leases cost more monthly, but can help frequent drivers avoid end-of-term charges

- Damage charges. You are responsible for damage beyond normal wear and tear.

- Early termination penalties. Ending a lease early can be expensive, even if you use a lease-transfer service.

Pros of Buying

- Ownership. Once the loan is paid off, the vehicle is yours.

- Resale or trade-in value. You can sell or trade the vehicle and use its value toward another car.

- More flexibility. You can sell or trade a financed vehicle at any time, as long as you pay off the loan balance.

Cons of Buying

- Higher upfront cost. Buyers often need a larger down payment, especially with weaker credit.

- Higher monthly payment. Loan payments are usually higher than lease payments for the same vehicle.

- Risk of being upside down. Depending on loan length, depreciation, and interest, you may owe more than the vehicle is worth for part of the loan term. After the warranty expires, repair costs are also your responsibility.

Leasing and Buying: Key Differences

You can draw some fairly strong contrasts between vehicle leasing and financing. Each offers both advantages and disadvantages. In the short term, leasing a car will cost less. However, two leases will cost more than buying one car in the long run. And at the end of the loan term, the vehicle will be paid off, and whatever value the car retains will be yours.

Here are some other differences.

| Leasing | Buying | |

| Monthly Payments | Usually lower | Usually higher |

| Early Termination | Often costly | Possible if you pay off the loan |

| End of Term | Return, buy, or extend the lease | Keep, sell, or trade the car |

| Mileage | Limits apply | No mileage limits |

| Customization | Restricted | Allowed, within warranty limits |

| Warranty | Often covers most or all of lease term | May expire before the loan ends |

| Credit | Best deals require strong credit | Weaker credit may require more money down |

Types of Leases

Closed-End Lease

A closed-end lease is the most common type. It sets the term, payment, mileage cap, and residual value upfront. If you meet the contract terms, you can return the car at lease-end. You may also have the option to buy it for a predetermined price.

Open-End Lease

An open-end lease places more risk on the lessee and is more common for businesses. If the vehicle’s market value is lower than the residual value at lease end, the lessee pays the difference. Open-end leases may offer more flexible mileage terms.

Single-Pay Lease

A single-pay lease requires all lease payments upfront. It can lower the money factor and total cost, and it may help shoppers with weaker credit qualify.

Can I Lease a Used Car?

Yes. Some dealerships lease used cars from its certified pre-owned vehicle inventory, usually newer models with factory warranty coverage and CPO benefits.

How Long Is a Car Lease?

Most leases last 24 or 36 months, though some advertised specials may run 39 months or longer. Longer terms can lower the monthly payment, but the difference may be modest.

Can a Car Lease Be Extended?

Yes. Many lessors allow month-to-month or fixed-term extensions. You will keep making payments and may need to sign an extension agreement.

Is It Possible to Lease a Car for One Year?

It is possible, but it can be expensive because vehicles depreciate quickly in the first year. A long-term rental or subscription-style car club may be a better short-term option.

Key Leasing Terms to Know

| Term | Definition |

| Acquisition Fee | A fee charged to set up the lease. It can be as much as $1,000 and is rarely negotiable. |

| Allowable Mileage | Also called the “mileage cap,” the annual mileage limit is in the lease. |

| Capitalized Cost | The agreed selling price of the vehicle plus any fees included in the lease. |

| Capitalized Cost Reduction | Any payment, trade-in allowance, or rebate that lowers the capitalized cost. |

| Depreciation | The vehicle’s lost value during the lease. |

| Disposition Charge | A fee charged at lease end to clean and process the returned vehicle. It may be waived if you buy the car or lease another vehicle from the same company. |

| Drive-off Fees | Amounts due at signing, including fees, deposits, taxes, and the first payment. |

| Early Termination | Ending the lease before the contract expires. This can trigger significant penalties. |

| Gap Insurance | GAP (guaranteed asset protection) coverage that helps pay the difference if the leased vehicle is stolen or totaled and insurance does not cover the full balance. |

| Lessee | The person leasing the vehicle. |

| Lessor | The company that is financing the lease. |

| Money Factor | The lease’s financing charge. Multiply by 2,400 to estimate an annual percentage rate. |

| Payoff Amount | The cost to buy the vehicle is usually tied to the residual value. |

| Term | The length of the lease. |

How to Lease a Car

- Check your credit score. Strong credit can help you qualify for better lease terms.

- Set your upfront budget. Know how much you can pay at signing, including fees and deposits.

- Estimate your annual mileage. Choose a mileage cap that matches your driving habits.

- Shop for vehicles with strong resale value. Higher expected residual value can lower the monthly payment.

- Compare lease offers. Review capitalized cost, money factor, fees, mileage cap, and end-of-lease charges.

Questions to Ask Before Signing

Here are questions to ask the dealership or other lessor before you leap.

- What is the residual value?

- What is the lease-end purchase price?

- What is the money factor, and what interest rate does it equal?

- Is there a payment grace period?

- What is the late-payment fee?

- What fees apply at lease end?

- What are the early-termination penalties?

- What counts as normal wear and tear?

- What is the charge for each excess mile?

Bottom Line on Car Leasing

Car leasing can provide lower monthly payments, a newer vehicle every few years, and warranty coverage during most or all of the term. But it also comes with mileage limits, no ownership equity, potential wear-and-tear charges, and costly early-termination penalties.

Leasing works best for drivers who want predictable short-term costs and newer vehicles. Buying is usually better for long-term ownership, flexibility, and building value in the vehicle.

Visit the Kelley Blue Book Affordability Hub to explore our curated articles designed to help you make smart, budget-friendly decisions.

Editor’s Note: We have updated this article since its initial publication.