The April 15 tax filing deadline this year can be either a source of worry for Americans who owe Uncle Sam money or a source of joy for those anticipating extra cash in their bank accounts. According to the IRS, the average tax refund in tax year 2024 was $3,167. This amount is nothing to scoff at, and may represent a significant chunk that could go towards buying a new vehicle. However, you should be careful before you make a new purchase with your return. Here are five mistakes to avoid when using your return to get a new or used car:

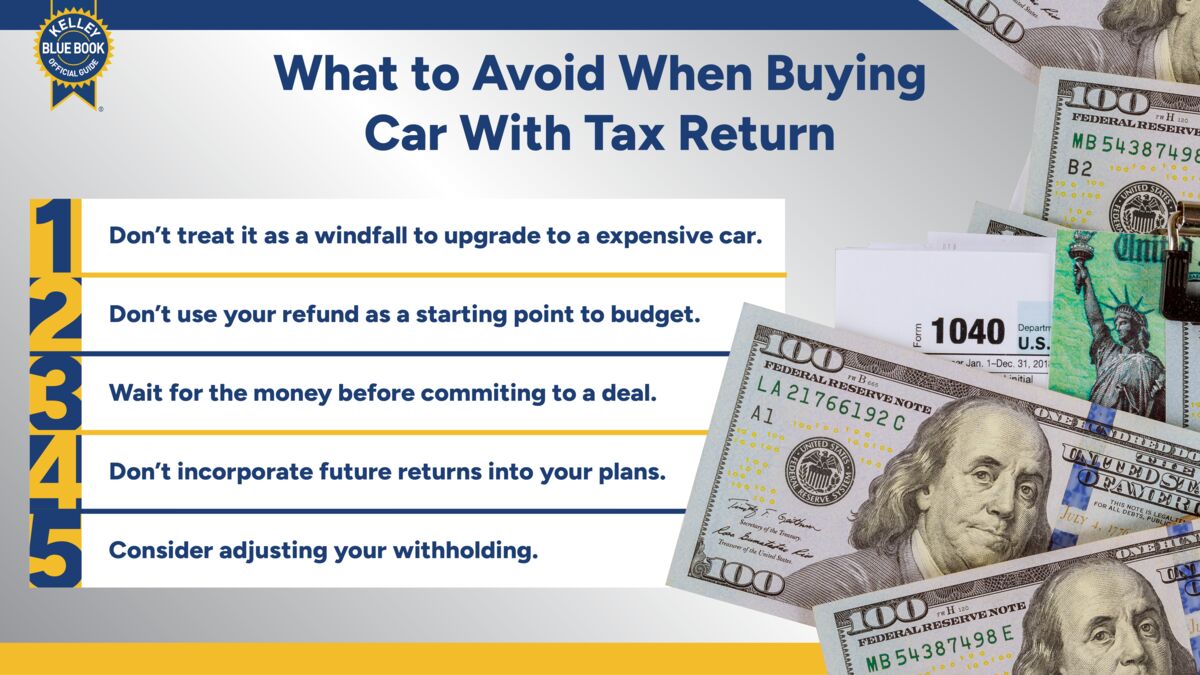

1. Don’t look at it as a windfall to upgrade to a more expensive car.

If you’ve been shopping for a vehicle before you figured out your tax refund, stick with that initial plan. Don’t use this cash as a rationale to upgrade to a more expensive vehicle. While your refund will certainly help with a car purchase, it is still a one-time payment. Getting a more expensive vehicle will translate to higher monthly payments for years to come, so you should still stick to what you can safely afford.

RELATED: Use Kelley Blue Book’s Affordability Calculator to see how much car you can afford.

2. Don’t use your refund as a starting point in figuring out the deal.

While an average refund may look significant as a lump sum, take that number and divide it by the number of anticipated payments you will make over the course of the loan or lease. That significant return suddenly looks a lot smaller when you consider how long you’ll be in the vehicle. By sticking to your original deal, you eliminate the risk of overextending your budget. The money you get from your refund will then seem like a real windfall in reducing your out-of-pocket expenses for the new vehicle purchase.

MORE: How Much Is the Typical Car Down Payment?

3. Wait until you have the check in hand before using it for the deal.

Don’t get ahead of yourself when considering a tax refund to be part of a deal. While you may be confident in your calculations on your return, the IRS may have other ideas. Wait until the check hits your account before committing to a deal that relies on the refund.

4. Don’t rely on your annual tax return as a recurring source of cash.

It’s better to treat your refund as a one-time deal. Although you could get the same amount of money next year, you never know what changes will occur to your situation or the tax code. Next year, you may get more, less, or even owe money compared to this year. It’s never a good idea to plan around something unknown.

MORE: Hidden Finance Costs When Buying a Used Car

5. Remember, it’s your money in the first place.

While receiving your tax refund may feel like free money, it is essentially a loan to the government at interest-free rates. Whatever you get in your refund this year, divide by 12 and see how you can use that extra money every month, rather than waiting until the following spring to get it back in a lump sum. By adjusting your withholding, you may find that making that monthly loan or lease payment may be a little less painful.

RELATED: Tax Time Car Buying

Editor’s Note: We have updated this article since its initial publication.