If you are in the market for a new car, a lump sum from your tax return can come in handy. While it may be tempting to spend a couple of thousand dollars more on a nicer car, we suggest using it as a tool, not as a lottery win. There are other things to consider, and the best use of that cash might actually be to split the lump sum over time.

Do Your Homework

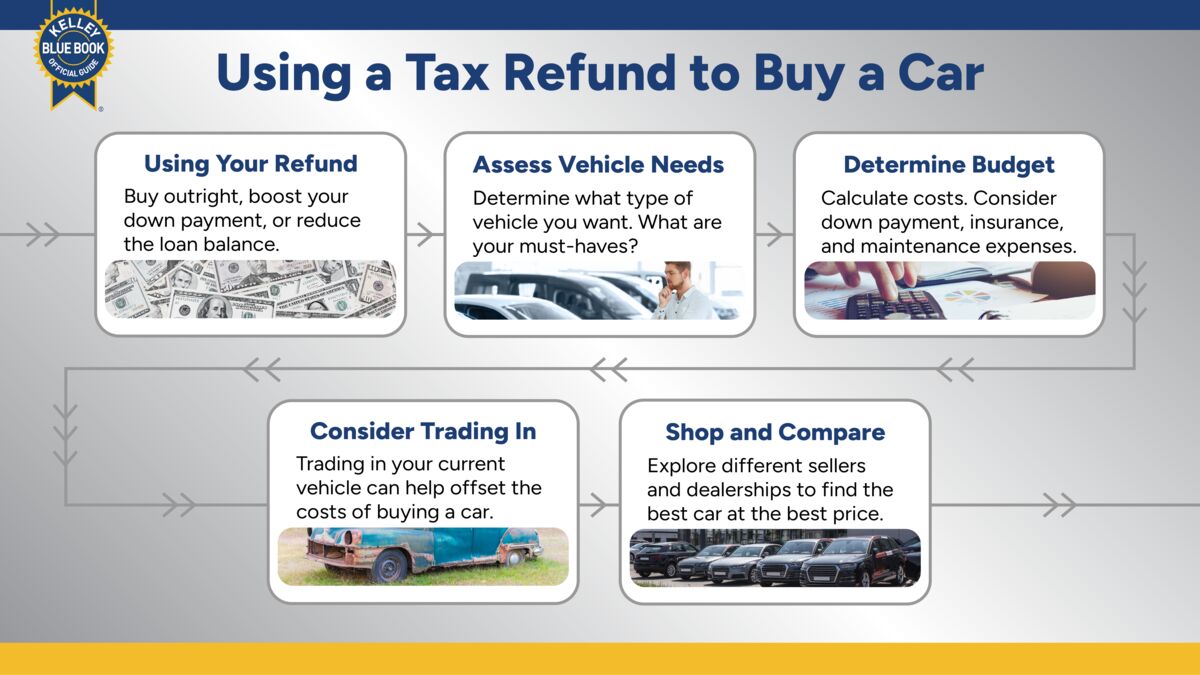

Having several thousand extra dollars on hand is a great motivator when shopping for a new vehicle. It’s tempting to put it all into a down payment for a fancier car. With all the deals and incentives floating around touting low or no down payments, you easily could find yourself pulled into a hastily arranged transaction. If you act too quickly, you may end up regretting the decision for years to come. Don’t let cash cloud your thinking.

Set the refund aside and look at what you can reasonably afford, not just in monthly payments, but in the total cost of the vehicle. This includes the down payment, insurance costs, maintenance, and depreciation. We recommend using tools like our 5-Year Cost-to-Own (5YCTO) calculator to get a good idea of your total price over time. Using 5YCTO as a comparison tool will enable you to choose the right vehicle for your budget.

What’s Your Trade-In Worth?

If you currently own a car, you can determine the value of that vehicle and use it as a trade-in. It represents some of the equity you’re bringing to the deal, and can help lower vehicle costs. We have tools at KBB to help you determine your vehicle’s value, so you can accurately assess what you can expect in a deal. Kelley Blue Book’s Instant Cash Offer (ICO) is another tool you can use to set a floor for the value of your current car. It allows dealers to bid on your vehicle and guarantee a trade-in or sale price.

Develop a Tax Refund Game Plan

As you put together your purchase plan, make sure to identify how much money you can bring to the deal. This includes the value of your trade-in, down payment, and financing options with your bank or credit union. Being pre-approved for a loan gives you leverage to ask the dealer if they can beat your guaranteed rate. At the same time, consult with your insurer to find out the coverage rates for the vehicle class you’re interested in.

Once you’ve figured out a budget, it’s time to shop, but that doesn’t necessarily mean visiting a dealership. You can do much of this legwork online, comparing different cars, features, lease deals, and purchase prices. Don’t rule out the used car market as well. Many manufacturers have Certified Pre-Owned (CPO) programs as a way to get into a class-above model at a price below the new car you’re considering.

The Dealer Visit

After you’ve collected all your information, it’s time to head to the dealer for a thorough test drive. Take time to learn the vehicle’s features with the sales representative so you’re comfortable and aware of what you’re buying. If you’ve been out of the market for some time, there’s a lot of new technology on board that you may be unfamiliar with. Take the time to become acquainted with these systems, which, while helpful, may have warnings or take actions that you may find annoying.

All the planning and preparation will contribute to a smooth purchase process. If you factor in your tax return cash after calculating all your expenses, you may find that you don’t need to put the whole amount down or that your monthly payments may end up being lower. Being informed will allow you to use your tax refund strategically. That way, the agreement doesn’t drive you; you drive the deal.

MORE: Top 5 Mistakes to Avoid When Using Your Tax Return to Buy a Car

Editor’s Note: We have updated the article since its initial publication.